The last few years have proved to be a pivotal period, full of opportunities for merchants looking to fine tune their subscription management.

Central to this change, SEPA Direct Debit stands out as the method of choice for recurring payments, promising to simplify financial processes and optimize the user experience for both merchants and consumers.

In this comprehensive guide, we take a closer look at the practical benefits of SEPA Direct Debit for subscription management.

From precise control of the payment process to a significant reduction in administrative time, we invite you to discover how this solution can act as a catalyst, propelling subscription management towards greater efficiency while strengthening customer relations at the same time.

Ready to find out how SEPA Direct Debit can help you optimize your subscriptions for the coming year? That’s what we propose to explore in detail.

What is the Single Euro Payments Area (SEPA)?

The SEPA or Single Euro Payments Area regulation marked an important step in the economic integration of Europe by creating a single euro payments area.

This system, launched in 2014, aims to harmonise cross-border financial transactions within the eurozone, thus facilitating trade and strengthening economic cohesion between the participating countries.

The idea of creating a single euro payments area emerged in the early 2000s as part of the European Union vision of a more integrated single market.

→ Before SEPA, cross-border transactions were often complex and costly due to the diversity of national systems.

This fragmentation hindered the fluidity of trade and financial transactions within the eurozone.

According to the economic-financial documentation centre at the Ministry of the Economy, Finance and Industrial and Digital Sovereignty of France: “The aim is to simplify procedures and reduce costs by enabling companies to centralise their payment management. SEPA Direct Debit applies to all companies, whatever their size or business sector, even if they have no international transactions.”

Consumers also benefit from faster, more efficient transactions, strengthening the European single market.

SEPA covers the 27 Member States of the European Union, the member countries of the European Economic Area, as well as Switzerland, Andorra, Monaco, San Marino and the Vatican City.

The members of the EEA (European Economic Area) are Norway, Iceland and Liechtenstein.

The Single Euro Payments Area regulation marked a significant step towards European economic integration by removing obstacles to cross-border payments in euros.

By promoting standardisation and simplifying processes, it has helped to create a more coherent and efficient financial environment within the eurozone.

What are the main provisions of the SEPA regulation?

The main provisions of the Single Euro Payments Area regulation are as follows:

- IBAN (International Bank Account Number): SEPA introduced the widespread use of the IBAN, an internationally standardised bank account number. This simplifies account identification and facilitates cross-border transactions;

- BIC (Business Identifier Code): the BIC, also known as the “SWIFT code”, is a unique identifier for financial institutions. Its use in this system guarantees precise identification of the banks involved in a transaction;

- the Numéro National d’Émetteur (which identified the creditor for domestic transactions) has been replaced by the SCI (SEPA Creditor Identifier). The Banque de France allocates this SCI on request via the bank;

- XML standards for transactions: this type of transaction requires the use of XML standards for the exchange of financial information between banks, thereby standardising payment processes and improving operational efficiency;

- credit transfers and direct debits: SEPA has established common standards for credit transfers and direct debits, enabling companies and consumers to make regular transactions in a harmonised way.

SCT vs. SDD: what is the difference between a SEPA credit transfer and a SEPA Direct Debit?

The SEPA Credit Transfer (SCT) and the SEPA Direct Debit (SDD), while sharing some similarities, differ in their nature and their use.

Here are the main differences between the SEPA Credit Transfer and the SEPA Direct Debit:

- Transaction initiator

A SEPA credit transfer is initiated by the payer (the sender or originator) who wants to transfer money from their own account to a beneficiary’s account.

In contrast, the SEPA Direct Debit is initiated by the creditor (the merchant in this case) to collect recurring payments from the account of the debtor (the consumer).

The creditor must obtain the debtor’s authorisation in the form of a direct debit mandate.

- Authorisation

For SEPA credit transfers, no specific authorisation is required on the part of the beneficiary.

The payer has full control over initiation of the payment.

For the SEPA Direct Debit, the merchant must obtain explicit authorisation from the consumer before initiating it.

This is done by means of a direct debit mandate signed by the consumer, authorising the withdrawal of funds from their account.

- Transaction frequency

SEPA credit transfers are generally used for one-off transactions, such as paying an invoice, making a refund, etc.

In contrast, the SEPA Direct Debit is designed for recurring payments, such as subscriptions, regular bills, loan repayments, etc.

- Payer’s control

The payer has direct control over each SEPA credit transfer initiated, as the payer must authorise each transaction.

For direct debits, the consumer retains a degree of control by being able to revoke authorisation at any time, thus eliminating the possibility of future direct debits.

What is the difference between the SEPA CORE Mandate and the SEPA B2B Mandate?

There are two main types of SEPA mandate: SEPA CORE (SDD CORE) and SEPA B2B (SDD B2B).

- SEPA CORE mandate

This is the standard type of mandate generally used for transactions between consumers and merchants.

It covers most SEPA direct debits, including those for regular transactions such as subscription payments, recurring bills and similar transactions.

Customers can request refunds for up to 8 weeks for authorised direct debits and 13 months for unauthorised direct debits (proof that the direct debit was unauthorised is required).

In terms of control, consumers can manage their direct debits on a case-by-case basis and create blacklists (blocking SEPA Direct Debits from certain merchants) and whitelists (authorising SEPA Direct Debits from certain merchants only).

They can also block all direct debits from their bank account.

- SEPA B2B mandate

It is specifically designed for business-to-business transactions.

It is used when the debtor is a company and the creditor is also a company.

While the SEPA B2B direct debit offers more limited protection, it provides better payment guarantees for merchants:

- In terms of notification, customers are informed in advance of each payment;

- In terms of refunds, customers are not entitled to any refund. On the other hand, there is a 13-month cancellation period for fraudulent transactions without a valid B2B mandate;

- Before debiting the payer’s account, the payer’s bank must ensure that each condition has been correctly met and approved by the payer and that the mandate information collected for each direct debit matches the information on the original mandate. The bank must also comply with any additional authentication instructions given by the payer. This is essential, given that there is no right to a refund.

SEPA B2B direct debits are more time-consuming to set up than SEPA CORE direct debits.

However, SEPA B2B offers a major advantage to the creditor, as it guarantees payment.

(Source: SlimPay)

What must a SEPA Direct Debit mandate contain?

According to the Banque de France website, a paper SEPA mandate must contain at least the following data:

- The heading “SEPA Direct Debit mandate”;

- The unique mandate reference (UMR) preferably provided as soon as it is issued by the creditor. If it does not appear on the copy sent to the debtor, it must be inserted on the mandate by the creditor (before archiving on paper) and communicated to the debtor before SEPA Direct Debit transactions are initiated;

- The creditor’s contact details: address and name/company name, or name/trading name if different;

- The SEPA Creditor Identifier (SCI);

- The following statements:

By signing this mandate form, you authorise (A) {NAME OF CREDITOR} to send instructions to your bank to debit your account and (B) your bank to debit your account in accordance with the instructions from {NAME OF CREDITOR}.

As part of your rights, you are entitled to a refund from your bank under the terms and conditions of your agreement with your bank.

A refund must be claimed within 8 weeks starting from the date on which your account was debited.

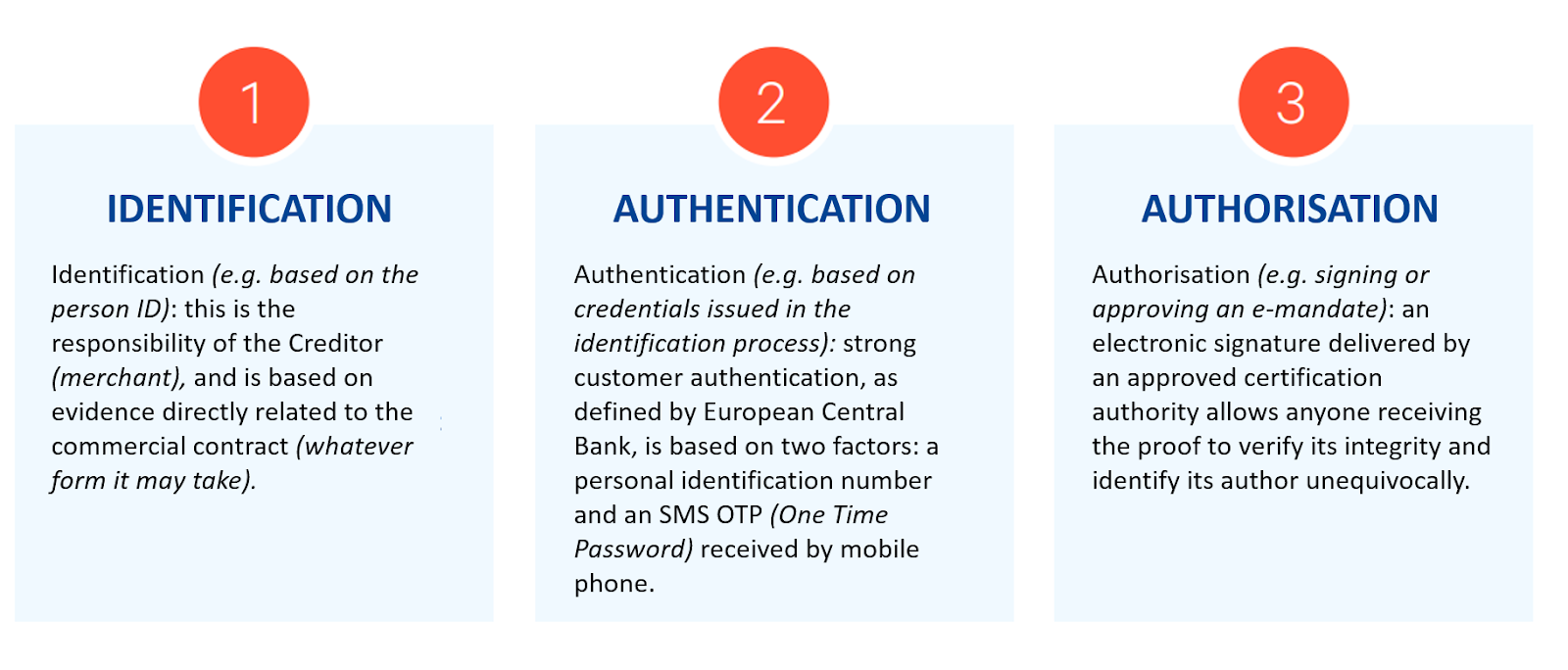

The e-mandate is the electronic format of this document.

It must be processed in a compliant manner in order to be legally binding and applicable in the event of a dispute.

→ At SlimPay, we have developed best practice for e-mandates, based on a three-stage approach: identification, authentication and authorisation:

The payment process has been designed to be seamless and optimized for smartphones and computers.

We have set up a digital mandate generation process, with pre-filled customer data:

- Automatic creation of a unique mandate reference (UMR) for each customer;

- Easy search for mandates and subscribers;

- Saves time by avoiding manual entry.

Our mandate library keeps everything in one place:

- Storage area for all mandates with an easily accessible interface;

- Two-tier archiving, including a legal compliance tier;

- Existing mandates can be imported via the dashboard.

There is also full automation using the API:

- Mandate generation;

- Creation of a single payment or a payment schedule;

- Electronic signature of mandates, etc.

What are the benefits of SEPA Direct Debit?

The use of this type of direct debit offers significant benefits to companies, helping to strengthen their financial and operational stability.

→ Facilitates recurring billing

This type of direct debit is particularly suitable for recurring billing, such as subscriptions or regular transactions with a fixed date.

Merchants offering services on a monthly, quarterly or annual subscription can automate customer payments, thus simplifying the billing and collection process.

→ Ensures payment deadlines are met and prevents payment incidents

By using the Single Euro Payments Area direct debit scheme, companies can ensure that payment deadlines are met.

This helps avoid payment incidents such as late payment, missed payment or partial payment.

By automating the direct debit process, the risks associated with human error or oversights are reduced, thus stabilising the merchant’s cash flow.

→ Facilitates identification of payments received

The SEPA Direct Debit makes it easier to manage financial transactions by clearly identifying the payments received.

Merchants can easily track and reconcile payments made with the corresponding invoices, thus simplifying accounting management.

→ Improves cash flow planning

By knowing the exact date when an invoice will be paid by direct debit, merchants can draw up more accurate cash flow plans.

This predictability facilitates cash flow management, enabling merchants to better anticipate their financial needs and optimize their investment, supplier payment and cash flow decisions.

→ Optimizes working capital requirements

The SEPA Direct Debit helps to optimize working capital requirements by improving the regularity and predictability of collections.

By reducing payment times and minimising delays, a company can better manage its financial resources and reduce its dependence on external sources of finance.

Why choose SEPA Direct Debit for your recurring payments?

Merchants who manage subscriptions or memberships can benefit significantly from the use of SEPA Direct Debit.

This payment method offers 3 key advantages that not only optimize the financial stability of companies, but also simplify their administration.

→ Gives control over payments

The SEPA Direct Debit gives merchants greater control over recurring payments.

By pre-authorising payments from the customer’s account, the SEPA Direct Debit provides merchants with the assurance that bills will be paid on time each month.

This enhanced control minimises the risk of missed payments on the customer’s side and ensures predictability in the receipt of funds for the merchant.

→ Optimizes administration

Using the SEPA Direct Debit results in a significant reduction in the administration time required to manage recurring payments.

By automating the direct debit process, merchants eliminate the need for frequent manual intervention when processing transactions.

This automation also simplifies the management of unpaid bills, reducing the time spent on sending reminders and facilitating bank reconciliations through the availability of structured information.

→ Maintains a high retention rate

One of the key advantages of the SEPA Direct Debit is that it eliminates declined payments due to incidents such as expired or lost payment cards.

By offering a reliable and consistent payment method, the SEPA Direct Debit strengthens customer loyalty over the long term.

Customers benefit from a fast, practical solution, without the hassle of frequently updating their payment details.

This reliability in the payment process helps to maintain a high retention rate, which is essential for creditors operating business models based on subscriptions or recurring payments.

Conclusion

It is clear that the SEPA Direct Debit, as a recurring payment method, has gone beyond its simple transactional role to become a genuine strategic opportunity.

It offers institutions, whatever their size and sector, the opportunity to optimize the management of their financial flows while enhancing the overall user experience.

The SEPA Direct Debit turns out to be much more than a means of ensuring that payment dates are met.

→ It is a major ally in reducing administrative time, helping to free up precious resources.

→ In addition, its ability to maintain a high retention rate reinforces its status as an essential tool in the dynamic field of subscriptions and recurring billing, foreshadowing its central role in the financial landscape.

The SEPA Direct Debit is a strategic lever for merchants moving towards more agile, customer-focused management.

It becomes a key catalyst for sustainable growth, offering a reliable solution for ensuring stable cash flow while fostering exceptional customer relationships.

The SEPA Direct Debit has confirmed its role as an essential partner for companies looking to manage their subscriptions and billing more efficiently and build high-quality customer relationships over the coming year.

Read also :

→ PSD1: what is it all about ?

→ PSD2: What is the impact on online payments ?

→ Payment data and GDPR: How can your customers be protected ?

→ Online payment: how do you manage the risk of fraud ?

→ IBAN fraud What can merchants do to prevent fraud ?